With corporate annual reports being finalized in the next couple of months, we are almost at the start of the next ESEF filing season. The ESEF mandate now moves into Phase II and companies will be required to ‘Block Tag’ the notes to their accounts apart from tagging the five primary financial statements. The latest ESEF Reporting Manual says text block tagging requirements start during the financial year 2022 and issues guidelines for companies to follow.

To briefly touch upon the more technical aspects of ESEF, the guidance states that report preparers must tag the disclosures in their financial statements that correspond to IFRS concepts on the list in Annex II of the Regulatory Technical Standards (RTS). However, issuers can voluntarily tag all the disclosures present in the annual financial report with elements other than in Annex II as present in the ESEF reference taxonomy.

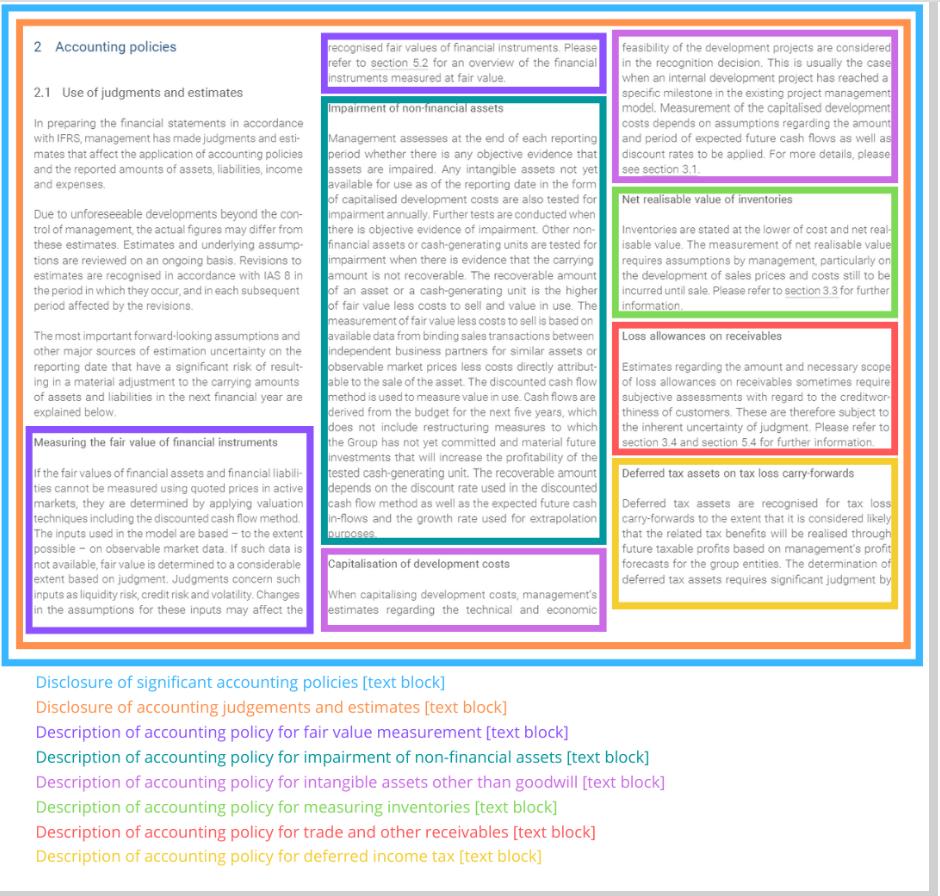

The Updated manual also provides essential guidance on how text block tags are to be constructed.

ESMA’s Recommendations for Block Tagging

Here are some recommendations on block tagging that are available in the ESEF Reporting Manual.

- The European Securities and Markets Authority (ESMA) recommends that the element ix:continuation or ix:exclude (Tagging a Disclosure in Different Sections of the Notes to the Consolidated IFRS Financial Statements) should be applied for marking-up multiple pieces of text to a single text block tag.

- ESMA also recommends that there should be the lowest level of granularity for block tagging the IFRS consolidated financial statements and individual tables contained within a single note. Therefore, issuers are not required to apply “textBlockItemType” elements from Annex II on selected rows or columns of such table and instead shall apply corresponding elements on the entire table.

- There is also no obligation to create an extension element to block tag notes and accounting policies. However, ESMA encourages the creation of extension elements for block tagging if a specific element is not present in the ESEF taxonomy.

- There is no obligation to anchor extensions in the notes to the financial statements. However, ESMA encourages anchoring those extensions to maintain consistency across reporting periods to the maximum possible extent.

Mandatory Elements and Markups

Below are a few relevant Annexures for the mandatory marking up of notes:

- Issuers shall, as a minimum, mark up the disclosures specified in Annex II (Just over 250 mandatory elements if applicable) where those disclosures are present in IFRS consolidated financial statements.

- Mandatory elements of the core taxonomy that need to be marked up include ~ 230 block tags for the Notes.

- The list of mandatory elements to be marked up (Table 2 Annex II) includes elements with different levels of granularity – wider and narrower elements that can be grouped by topic.

- One note could be block-tagged with several mandatory elements (multiple and/or embedded tagging)

Warnings for Mandatory Elements and Mark-ups

The validation of ESEF reports is based on the rules published in the reporting manual. In some cases, there are errors or warnings that do not reflect any real issue in the report. This may cause preparers to make undesirable modifications to their report to resolve the error or warning. Hence, it helps preparers to ignore errors or warnings that lead to real validation errors being ignored. We are happy to see several changes in the reporting manual that seek to reduce the number of false positive errors and warnings in validation results.

Conditional Mandatory Elements

Warning – A major cause for false positive warnings is the need to report “mandatory” elements which are not relevant in a particular report. For instance, if a company changes its name, it becomes mandatory to tag an explanation for the name change. But most of the time, when a company has not changed its name, this disclosure is not required. The absence of the explanation tag will be flagged as a warning, even if the company has not changed its name. The updated reporting manual clarifies that mandatory elements (listed in RTS Annex II) need to be tagged only if the corresponding disclosures are present in the AFR. Further, it says filers need not include unnecessary disclosures solely to satisfy mandatory element tagging rules or indicate that such disclosures are not present.

Error – Although there are 10 mandatory elements which are required to be tagged as per ANNEXX II of RTS in the annual report, among those if we are not tagging 9 elements it will throw the false positive warnings but if the element “Name of reporting entity or other means of identification” is not tagged then it will give you an error which will result in restricting the filer to file the iXBRL files with the regulator. Issuers are advised to give the correct information for all the 10 mandatory elements to the vendors from the report.

Challenges Faced

Currently many service providers are facing technical challenges with regard to Phase II block tagging. The biggest challenge is multi-layer or nested tagging, application of continuation/exclude tags (tagging a disclosure in different sections of the notes to the consolidated IFRS financial statements), and retaining the formatting of the xHTML document in block tags. We are very happy to share that IRIS Carbon is ready with all the latest updates and phases for the upcoming filing season.